Knowledge Centre - Resources

The Psychology of Investing: Understanding How Financial Decisions are Made.

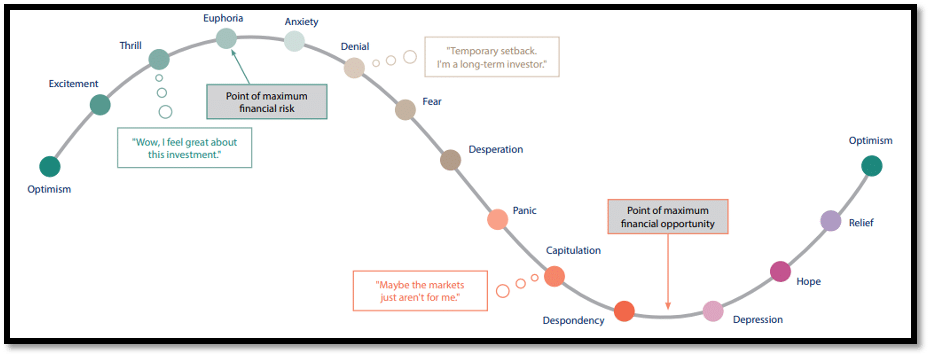

Most investors would agree that fear and greed move the market. They are often considered the driving forces behind investment behaviour, such as during the tech bubble of the late 1990s, when greed prevailed, or during the 2008 financial crisis when fear dictated all actions.

Although true, using fear and greed to characterise all investors’ behaviour is far too simplistic. Our mind is so sophisticated, and human emotions are way too complex, that fear and greed do not adequately describe the psychological bias that affects us when we make investment decisions.

Are all investors perfectly rational?

Risk aversion bias is one example of psychological bias that inhibits rationality; suppose if you decide to set up a pension investment plan. You must decide whether to contribute, how much to contribute, and how to allocate the investment to various asset classes. Given your pension plans’ importance, how would you frame your decision in ways that foster optimal choices?

Unfortunately, most people do not know what level of risk is appropriate for them. Because they are unsure, they tend to be extremely risk averse. If you don’t know what level of risk you should take, you would probably pick the one you perceive to be the most moderate option. But is that really the value-maximizing decision? And were you rational in making it? Emotions are another natural inhibitor of your rationality. When markets are moving quickly – either upwards or downwards- it is tempting to make impulsive decisions that seriously threaten your long-term financial health.

If markets were to enter a recession today and you found yourself with a -30% drawdown in your portfolio, would you immediately divest your investments? Such emotion-driven behaviour contradicts the investment mantra ‘buy low, sell high’. Investing based on emotion is the main reason why so many people are buying at market tops and selling at market bottoms.

But what if I told you that the worst average annualized return for the stock market is actually positive? This may sound counterintuitive, but the table below will provide an answer.

Using the S&P 500 as our sample, the table below calculates the highest, lowest, and average annualized returns for the specified period between Jan 1926 – Jul 2023.

Source: FE Analytics, All returns in USD

Over the period of almost a century, the worst average annualized return you could get is from a 5-year period with an annualized return of 10.26%. Surely, it’s not all stars and rainbows in all investment portfolios, but over the long term (20 years), a century of history has shown that you generally see positive returns in your investments.

Some general rule of thumb to keep in mind when investing.

Certainly, there are risks in investing, but the risk is the price of admission for a higher reward. Likewise, when there is no risk, there is little reward. The key is retaining a long-term perspective, which protects against impulsiveness or irrational decision-making. We offer tips/advice below when starting or continuing your investment journey.

- Avoid suspect investment plans both on and offline. These are typically where you see investments offering outrageous returns, sometimes to the extent of 1000%. Most of them are investment scams rather than legitimate investment schemes, these schemes appeal to your ‘greed’.

- The News media, Chat rooms, message boards, and Twitter advice are for entertainment purposes only. These are where your overconfidence is fostered, familiarity is magnified, and artificial “social consensus” is formed. They enhance your psychological bias of ‘herd mentality’ but not your rationality if you are not mindful of it.

- Practice Mindful Investing, mindful investing involves being aware of one’s emotional and cognitive biases and taking deliberate steps to manage them. Adhering your investment plans to a long-term perspective can also help to avoid being overly influenced by short-term market fluctuations.

- Before you decide to invest, remember that it is unlikely that you know more than the market. Investing involves many aspects that are out of your control. Consulting a financial advisor for a more professional opinion may help in your quest for successful investing.

- Strive to diversify. Most concentrated investing is motivated by the desire to earn a higher return than everyone else is. The strategies for earning a higher return usually foster psychological biases and ultimately contribute to lower returns. However, the strategies for earning a reliable return, like fully diversifying, are successful because they inhibit your biases.

Investing is more than just numbers.

Successful investing is more than just understanding stocks and projecting financial numbers. Indeed, understanding yourself is equally important. “Knowledgeable” investors frequently fail because they allow their psychological biases to control their decisions.

Since investing goes far beyond just numbers and financial analysis. The decisions we make as investors are often influenced by a complex interplay of psychological factors. Understanding the psychology of investing is key to becoming a successful and resilient investor.

Recomended

Building a Resilient Portfolio During Volatility

Building Resilient Portfolios in Times of Market Volatility Market volatility is inevitable. But when the headlines turn red

Maximising Your Wealth as an Australian Expat in Singapore

Financial Planning for Australian Expats in Singapore Living and working in Singapore offers Australian expats unique financial advantages.